A practical 90-day framework to transfer authority, records, and beneficiary communication without governance gaps.

Trustee transitions fail when families treat them like paperwork instead of an operating handoff.

A clean transition is not just moving accounts. It is moving authority, decision logic, beneficiary expectations, and advisor coordination into one repeatable system.

If you are replacing a trustee or moving from an individual trustee to a professional model, use this 90-day framework to avoid delays, disputes, and rework.

Why transitions break

Most breakdowns come from four gaps:

- Authority is legally transferred, but decision workflows are not.

- Historical files arrive in fragments, not in an audit-ready package.

- Beneficiaries are notified too late or with vague language.

- CPA, attorney, and investment advisor handoffs are informal.

The result is predictable: distribution slowdowns, inconsistent messaging, and avoidable friction in the first quarter.

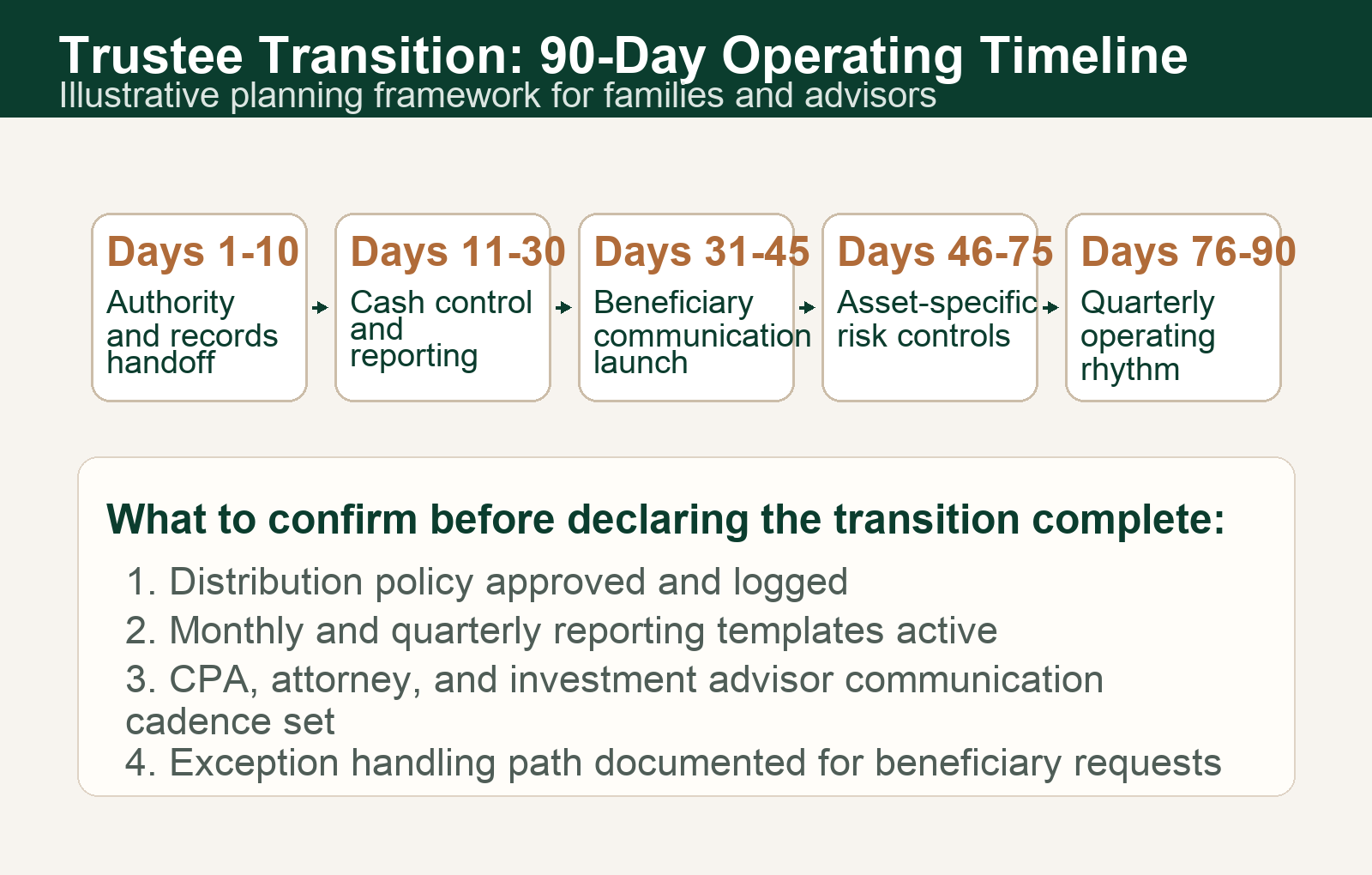

The 90-day transition framework

Phase 1 (Days 1-10): control and records

Objectives:

- Confirm governing documents, acceptance authority, and key dates.

- Freeze ad hoc exceptions until process controls are active.

- Inventory all accounts, entities, and outstanding requests.

Deliverables:

- Authority map (who approves what).

- Consolidated document index.

- Immediate-risk register.

Phase 2 (Days 11-30): cash and reporting baseline

Objectives:

- Establish distribution intake and approval path.

- Align cash forecasting with investment operations.

- Define monthly reporting package.

Deliverables:

- Distribution request form + decision log.

- 13-week liquidity view.

- Beneficiary reporting template.

Phase 3 (Days 31-45): communication reset

Objectives:

- Set one communication standard for all beneficiaries.

- Clarify timing and scope for updates.

- Reduce inbound confusion through proactive outreach.

Deliverables:

- Standard communication cadence.

- FAQ for common process questions.

- Escalation path for exceptions.

Phase 4 (Days 46-75): complexity controls

Objectives:

- Add controls for trust-owned entities, real estate, and concentrated positions.

- Define cross-functional review triggers.

Deliverables:

- Special asset governance checklist.

- Exception policy for non-standard requests.

Phase 5 (Days 76-90): lock operating rhythm

Objectives:

- Move from transition mode to steady-state governance.

- Confirm ownership and SLAs across trustee, advisor, CPA, and counsel.

Deliverables:

- Quarterly operating calendar.

- KPI baseline (response time, cycle time, exception rate).

Transfer package checklist (minimum viable)

| Area | Minimum package | Owner |

|---|---|---|

| Legal docs | Governing trust docs, amendments, acceptance records | Counsel + trustee |

| Financial records | Prior statements, distribution history, open obligations | Trustee ops |

| Tax | Prior returns, K-1 workflow, estimated payment plan | CPA |

| Advisor workflows | Liquidity protocols, rebalance constraints, cash windows | Investment advisor |

| Beneficiary communications | Contact matrix, prior notices, unresolved issues | Trustee relationship lead |

Transition SLAs worth setting early

Set these before day 30:

- Standard response time for inbound beneficiary requests.

- Maximum cycle time for routine distribution decisions.

- Turnaround window for CPA/counsel document requests.

- Escalation response standard for high-priority issues.

Without explicit SLAs, families often experience inconsistent service quality during the most sensitive period.

What families should ask on week one

- What is the exact workflow from request intake to final decision?

- Where are exceptions documented and approved?

- Which reports are delivered monthly vs quarterly?

- How do trustee, advisor, CPA, and attorney share updates?

- Who is accountable when timing slips?

If those five answers are not clear in writing, the transition is not complete.

Practical next step

If your family is preparing a trustee change in Overland Park or elsewhere, start by stress-testing your handoff process before documents move.

Use the Trust Audit Scorecard to identify your highest-risk transition gaps, or contact our team for a working session.

Educational content only; not legal, tax, or investment advice. Consult qualified professionals for guidance.