How to define trustee, advisor, CPA, and attorney responsibilities with a practical cadence and accountability map.

Most directed trustee structures underperform for one reason: roles are defined legally, but not operationally.

Families assume everyone knows who owns each decision. In practice, trustee, advisor, CPA, and attorney teams can all believe they are "supporting" the same issue while nobody is accountable for closure.

This guide gives you a practical operating template to make a directed structure fast, clear, and defensible.

When a directed model is a strong fit

A directed trustee structure usually works best when:

- You want to retain a trusted investment advisor.

- The trust needs professional administration and beneficiary communication.

- Asset complexity requires better process controls.

- You want cleaner separation between investment discretion and fiduciary administration.

Where confusion usually starts

- Cash management is split but not coordinated.

- Distribution decisions are approved without consistent documentation.

- CPA requests are routed through the wrong party.

- Beneficiary updates are duplicated or contradictory.

Each of these is fixable with a responsibility map and operating cadence.

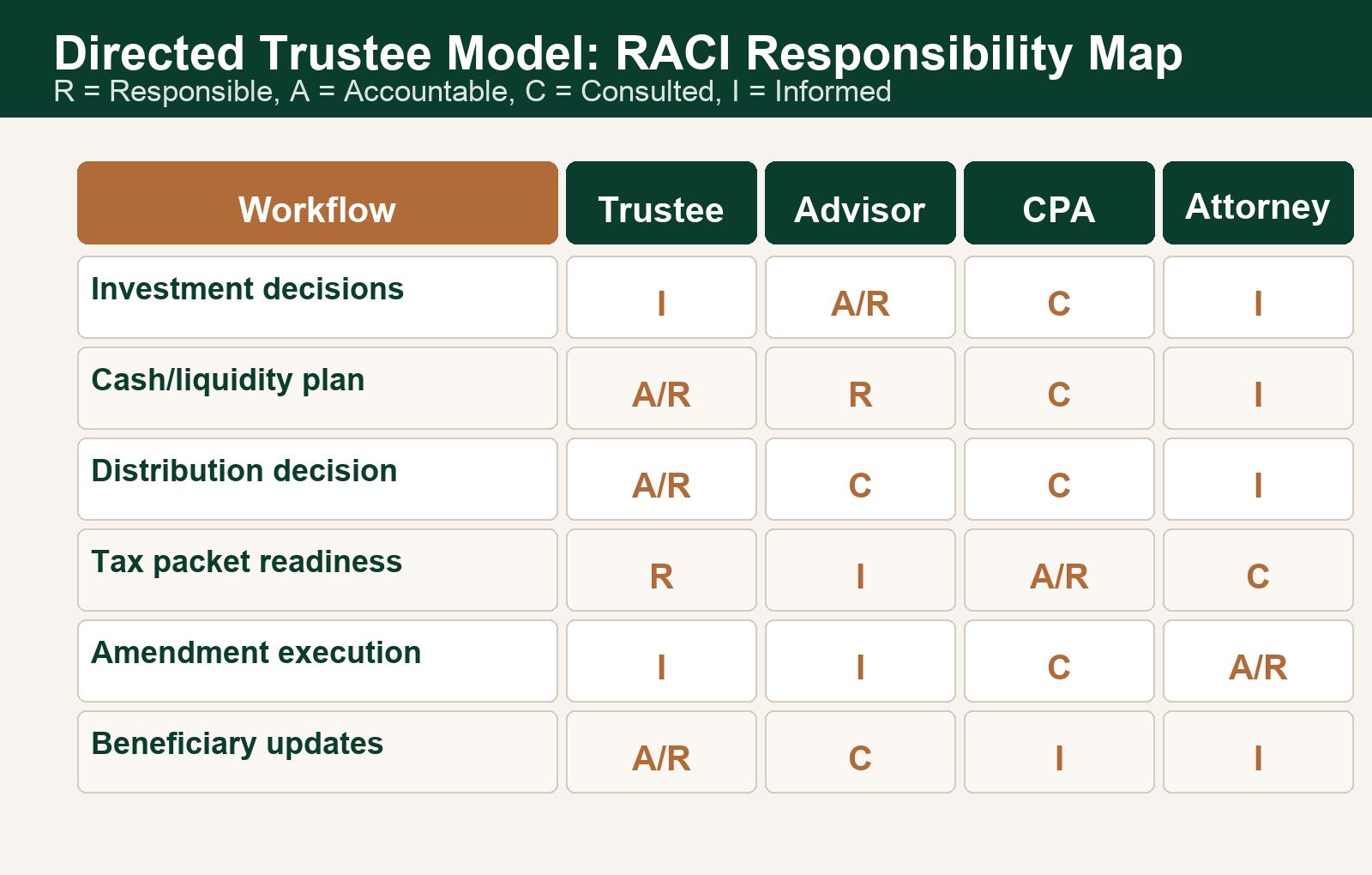

RACI template for directed trustee teams

| Workflow | Trustee | Investment Advisor | CPA | Attorney |

|---|---|---|---|---|

| Portfolio decisions | I | A/R | C | I |

| Cash and liquidity planning | A/R | R | C | I |

| Distribution approvals | A/R | C | C | I |

| Tax package readiness | R | I | A/R | C |

| Amendments and legal updates | I | I | C | A/R |

| Beneficiary communications | A/R | C | I | I |

RACI definitions:

- R: Responsible for execution.

- A: Accountable for final outcome.

- C: Consulted before decision.

- I: Informed after decision.

The cadence that keeps the model healthy

Weekly (30 minutes)

- Cash position and upcoming obligations.

- Pending distribution requests.

- Exceptions that may require cross-team review.

Monthly (60 minutes)

- Reporting quality and timing review.

- Tax readiness checkpoints.

- Beneficiary communication status.

Quarterly (90 minutes)

- Policy drift review.

- Concentration or liquidity risk review.

- Role boundary adjustments if process friction appears.

Service-level standards to agree in writing

- Initial response to beneficiary requests: under 1 business day.

- Routine distribution decision cycle: target 3 to 5 business days.

- Exception-case escalation acknowledgment: same business day.

- Monthly reporting release: fixed date window.

These standards are not marketing copy. They are operating controls that reduce conflict.

Implementation checklist (first 30 days)

- Approve one-page RACI signed off by all four parties.

- Publish one distribution decision log format.

- Set recurring weekly/monthly/quarterly calls.

- Assign one accountable owner for beneficiary communication.

- Test one complex scenario (for example: large discretionary distribution + liquidity event).

Practical next step

If you are deciding whether a directed model is right for your trust, run a structure check before onboarding.

Start with the Trust Audit Scorecard, then schedule a consultation to map a clean handoff for your advisor team.

Educational content only; not legal, tax, or investment advice. Consult qualified professionals for guidance.